All Categories

Featured

Table of Contents

[/video]

When the main annuity holder passes away, a selected beneficiary remains to get either 50% or 100% of the income forever. 60 years 6,291.96 6.29% Standard Life 65 years 6,960.24 6.96% Canada Life 70 years 7,776.60 7.78% Canada Life 75 years 8,941.56 8.94% Canada Life The current finest 50% joint life annuity price for a 65-year-old man is 6.96% from Canada Life, which is 0.24% less than the very best rate in February.

describes the individual's age when the annuity is established. These tables reveal annuities where revenue repayments remain degree throughout of the annuity. Escalating strategies are also available, where settlements begin at a reduced degree but enhance each year according to the Retail Rates Index or at a set rate.

For both joint life instances, numbers revealed are based on the first life being male, and the recipient being a female of the very same age. Single life, level 7,545.60 7,554.12 7,458.72 7,496.40 7,435.08 7,444.92 Single life, intensifying at 3% 5,390.40 5,399.16 5,341.80 5,425.80 5,673.36 5,535.84 Solitary life, intensifying at RPI 4,795.92 4,804.80 4,722.96 4,778.28 5,067.96 4,946.16 Joint life 50% 6,952.92 6,960.96 6,834.12 6,896.76 7,143.84 7,064.64 Joint life 100% 6,385.68 6,392.64 6,262.92 6,318.60 6,683.76 6,691.80 Information on historical annuity prices from UK suppliers, produced by Retired life Line's internal annuity quote system (commonly at or near the initial day of each month).

Furthermore: is where repayments start at a lower degree than a level strategy, however increase at 3% every year. is where payments start at a lower level than a level plan, yet boost yearly in line with the Retail Price Index. Utilize our interactive slider to reveal exactly how annuity prices and pension plan pot dimension impact the earnings you could receive: Annuity prices are a vital consider establishing the degree of income you will obtain when buying an annuity with your pension cost savings.

The higher annuity rate you protect, the even more income you will certainly obtain. For instance, if you were purchasing a life time annuity with a pension fund of 100,000 and were offered an annuity rate of 5%, the annual income you get would certainly be 5,000. Annuity prices differ from supplier to supplier, and service providers will certainly use you a personal rate based upon a variety of variables including underlying financial variables, your age, and your health and wellness and way of living for lifetime annuities.

This provides you certainty and confidence concerning your long-term retired life revenue. You can have a rising lifetime annuity. This is where you can choose to begin your settlements at a reduced degree, and they will certainly after that increase at a set percent or according to the Retail Cost Index.

In Plan Annuities

With both of these alternatives, when your annuity is set up, it can not usually be altered. If you pick a fixed-term annuity, the rate stays the exact same till completion of the picked term. Nonetheless, you can schedule your routine repayments to be increased according to the Retail Rate Index, as above.

It may amaze you to discover that annuity prices can vary significantly from provider-to-provider. Actually, at Retirement Line we have found a distinction of as long as 15% in between the lowest and highest possible prices readily available on the annuity market. Retirement Line is experts in providing you a comparison of the most effective annuity rates from leading service providers.

(also recognized as gilts) to fund their clients' annuities. This in turn funds the routine income settlements they make to their annuity clients. Carriers fund their annuities with these bonds/gilts since they are among the best types of financial investment.

When the Financial institution Rate is reduced, gilt yields are also low, and this is mirrored in the pension plan annuity rate. On the various other hand, when the Financial institution Rate is high, gilt yields and typical annuity prices likewise often tend to increase.

Annuity providers utilize added economic and business aspects to determine their annuity rates. The vital thing to bear in mind is that annuity rates can alter often.

Best Annuities Barrons

This was certainly great information to individuals who were prepared to transform their pension pot into a surefire income. In October 2022, Canada Life reported that normal annuity rates had struck a 14-year high increasing by 52% in the previous nine months alone. Canada Life's record during that time discussed a benchmark annuity for a 65-year-old making use of 100,000 to purchase an annuity paying an annual lifetime income of 6,873 annually.

They will instead base it on your specific personal conditions and the kind of annuity you wish to take. As we have explained above, your annuity supplier will base their annuity rate on economic and business variables, consisting of current UK gilt yields.

Annuity Board Of The Southern Baptist Convention

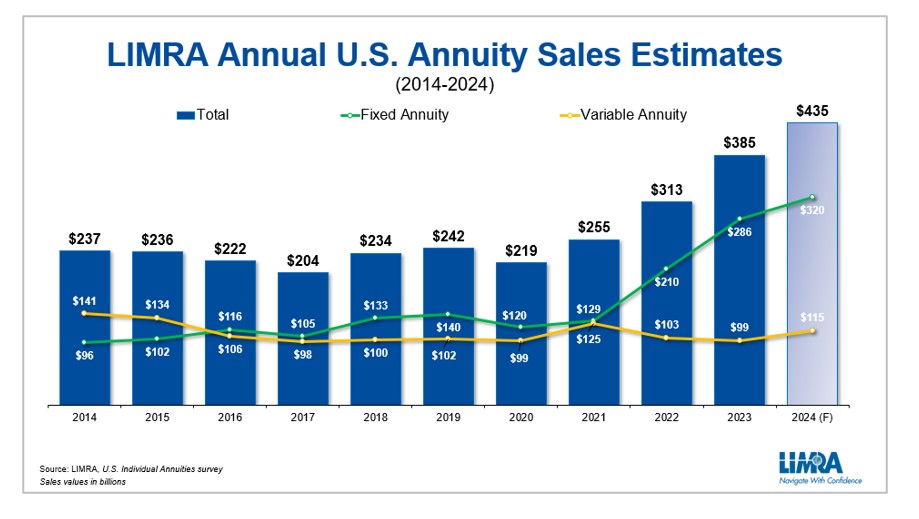

To put this right into viewpoint, that's almost dual the sales in 2021. In 2025, LIMRA is projecting FIA sales to go down 5%-10% from the record embeded in 2024 yet continue to be above $100 billion. RILA sales will certainly mark its 11th successive year of record-high sales in 2024. Investors thinking about safeguarded growth paired with continued solid equity markets has actually made this product in need.

LIMRA is forecasting 2025 VA sales to be degree with 2024 results. After record-high sales in 2023, earnings annuities moved by engaging demographics fads and attractive payout prices should go beyond $18 billion in 2024, establishing another record. In 2025, reduced rate of interest will certainly oblige providers to drop their payment rates, causing a 10% cut for earnings annuity sales.

Payout Annuity Formula

It will be a combined outlook in 2025 for the overall annuity market. While market problems and demographics are really desirable for the annuity market, a decrease in interest rates (which thrust the amazing development in 2023 and 2024) will damage fixed annuity products continued development. For 2024, we anticipate sales to be greater than $430 billion, up between 10% to 15% over 2023.

The firm is also a struck with representatives and clients alike. "They're A+ rated.

The company rests atop one of the most recent edition of the J.D. Power Overall Customer Satisfaction Index and flaunts a solid NAIC Grievance Index Rating, too. Pros Market leader in customer contentment More powerful MYGA prices than some other very rated companies Cons Online item info could be stronger Much more Insights and Specialists' Takes: "I have never had a poor experience with them, and I do have a pair of happy clients with them," Pangakis claimed of F&G.

The business's Secure MYGA includes advantages such as cyclists for incurable ailment and nursing home confinement, the capacity to pay out the account worth as a survivor benefit and rates that exceed 5%. Couple of annuity business succeed more than MassMutual for clients that value economic strength. The business, established in 1851, holds a prominent A++ rating from AM Ideal, making it among the most safe and strongest business available.

Its Secure Trip annuity, for example, provides a traditional means to create earnings in retirement coupled with convenient surrender charges and numerous payment choices. The firm additionally advertises registered index-linked annuities with its MassMutual Ascend subsidiary.

Sseu 371 Annuity Fund

"Nationwide stands apart," Aamir Chalisa, basic manager at Futurity First Insurance coverage Team, told Annuity.org. "They've obtained incredible customer support, an extremely high rating and have been around for a number of years. We see a great deal of customers requesting for that." Annuities can supply considerable worth to possible clients. Whether you want to produce income in retirement, grow your money without a great deal of danger or make the most of high rates, an annuity can efficiently accomplish your goals.

Annuity.org laid out to identify the top annuity firms in the market. To attain this, we developed, examined and applied a fact-based method based on crucial market variables. These include a firm's monetary strength, schedule and standing with customers. We additionally called several sector specialists to get their tackles different business.

{kind=link}

Latest Posts

Variable Annuity Rider

New York Life Immediate Annuity Rates

Growing Annuity Example